The scene of lending in Bangladesh is experiencing rapid shifts. Especially concerning online loan applications and consumer awareness. While digital lending promises quick financial answers, a critical trend has emerged: a sharp increase in online loan scams and (at least in my face) high-interest rate complaints. People are gradually wary, sharing experiences on social media platforms like Reddit and X about fraudulent schemes, exorbitant interest rates, (not even kidding) and aggressive collection tactics. This trend reveals a major concern for individuals seeking credit in Bangladesh, above all. When many are looking for financial assistance for things like education (and that says a lot) or personal needs.

Key Takeaways

- Online loan scams in Bangladesh are on the rise, with fraudsters misusing names of legitimate institutions like Bangladesh Bank and the World Bank.

- High interest rates and hidden fees from online loan apps are a major complaint among users.

- Many individuals face aggressive debt collection practices from unregulated digital lenders.

- There's growing skepticism towards quick online loan offers, pushing people towards traditional banking or regulated non-banking financial companies (NBFCs).

- Lack of clear regulatory oversight for all online lending platforms remains a significant issue.

Online Loan Scams Surge in Bangladesh

Online loan scams are currently a major problem in Bangladesh. With quite a few most of us falling victim to deceptive practices. As it turns out, this trend is alarming, prompting warnings from both Bangladesh Bank and the World Bank. Fraudulent groups are build fake websites, social media pages. Mobile apps that look like official financial institutions. They even use logos and names of reputable entities, like the central bank or the International Monetary Fund (IMF), to trick people into trusting them.

Many scam apps promise loans with super low interest rates or instant approval to attract desperate people. The catch? Now, they demand "processing fees" or "insurance" upfront, which is a big red flag. These fake platforms regularly illegally collect sensitive personal details, including names, gets at, dates of birth, mobile numbers, email handles, and National Identity (NID) card numbers, pretending these are for loan processing. This collected information is then used for identity theft. In many cases, it’s pretty scary how easily — well, actually, these scammers can steal your information, isn't it? The Bangladesh Bank has clearly stated that neither they nor the IMF are connected to these fake platforms. Com. Operating any loan platform without central bank permission is against the law, potentially leading to five years in prison or a fine of Tk 50 (seriously) lakh, or both.

Skyrocketing Interest Rates and Hidden Fees Plague Borrowers

Quite a few folks using online loan apps in Bangladesh are finding themselves — or rather, in a tough spot because of extremely high interest rates and hidden charges. This issue is a hot topic, or rather, showing up in online discussions and complaints. It truly makes you wonder. If some of these platforms is meant to help or simply trap everyone. 00% for a mix of categories like education, medical, or other personal expenses. 50% interest.

This brings us back to what we started with, however, some online apps charge much more. You might see rates as high — or rather, as somewhere around 22% or even higher. Actually, here's a better way to look at it — with additional processing fees that can take a big chunk out of the loan right from the start. Like, one Reddit user shared a deal with with an app offering a loan at over 22% interest, with a big amount disappearing as processing fees. This makes the actual amount received much less than what was borrowed, while the repayment amount remains based on the full sum. Some unregulated platforms can even hit you with daily interest additions if payments are missed. Leading to rates up to 60% of the borrowed amount in some extreme cases. This is a huge burden for anyone trying to manage their finances.

Interest Rate Comparison for Personal Loans (Approximate)

| Lender Type | Average Interest Rate (Annual) | Hidden Fees | Transparency |

|---|---|---|---|

| Traditional Banks | 13.00% – 16.00% | Low | High |

| Regulated Online NBFCs | 16.00% – 20.00% | Moderate | Fair |

| Unregulated Loan Apps | 20.00% – 60.00%+ | High | Very Low |

This table, if you look at it, makes the choice pretty clear, right? Com/decoding-bangladeshs-loan-app-craze/), comparing these rates is key.

Aggressive Tactics and Harassment from Loan Apps

Beyond the high costs, a disturbing trend involves the aggressive. And unethical debt collection practices of certain online loan apps. People all the time share terrifying accounts on social media platforms about (which, let's be honest, is a bit weird) how these apps operate. It can get pretty ugly. Many online loan apps demand access to personal data like contacts, galleries, and location upon installation. If a borrower falls behind on payments. These apps constantly use the collected personal information to harass not just the borrower, but also their contacts. This could involve threatening messages, shaming tactics. Or even spreading false information on social media. One Reddit post mentioned a user’s social media being flooded with messages calling them a "scammer". After a slight delay in payment, even involving their friends not (at least — that's what the data says) listed as references. This sort of public shaming is incredibly damaging.

The threats sometimes include sharing fake explicit photos or other sensitive images to contacts, even if these threats a lot aren't carried out. However, the fear and humiliation are real; one user recounted being told their account was "frozen" and then being asked for more money, even after trying to cancel the loan. In a tough financial spot, this highlights a big issue. Many of these apps prey on people who are already. As far as I know, but many have found that blocking, I mean, these numbers or refusing to engage can eventually make them stop.

Skepticism and the Search for Safer Lending

A growing sense of caution is spreading among people in Bangladesh regarding online loan apps. If you think about it, after so many stories of scams and rough experiences. Individuals are understandably hesitant to trust promises of blazing cash. This skepticism is good, actually. Many are now looking for safer options, realizing that a rapid loan might come with huge hidden costs or even lead to identity theft. Honestly, sometimes the old ways are the best ways, or at least, the safest.

When you look closely, people are starting to suggest turning to classic banks. And regulated financial institutions first, even if it means a longer process. Banks in Bangladesh offer a range of personal, home, and student loans with more transparent terms and stable interest rates. 75%; student loans, especially for those looking to study abroad, constantly require family cosigners or collateral through local banks. However, some global lenders are emerging that focus on a student's program. And earning potential instead of family collateral, which is pretty cool if (if you're into that sort of thing) you think about it.

There's a clear move away from unregistered apps towards platforms with regulatory backing. Like those regulated by the Bangladesh Bank. Com/personal-loan-in-bangladesh/) without falling into traps.

Common Mistakes Borrowers Make

Think of it this way. For loans, especially online ones, it's a breeze to trip up. One of the biggest mistakes people make isn't reading the fine print carefully — or at all; and honestly, quite a few online apps bury high processing fees or prepayment penalties in their terms, which can surprise you later. You might think you're getting a good deal. But the actual cost is much higher than expected. Another common blunder is giving these apps too much access to your phone data. They ask for contacts, location, and gallery access. And folks a lot grant it without thinking twice. This opens the door for harassment if you miss a payment. But then again, it depends.

Rushing into a loan mainly because of urgency is another trap, and let me tell you, scammers constantly create a sense of emergency, pushing you to make quick decisions without proper research. You might feel desperate, but that's exactly when you need to slow down. Always verify the lender's legitimacy. Check if they're licensed by Bangladesh Bank, if an offer seems too awesome to (which is exactly what you'd expect) be true, it probably is. If you think about it, finally, paying upfront "processing fees" for a loan that hasn't been disbursed is a massive red flag. And a classic scam tactic. Real lenders deduct fees from the loan amount itself, not demand separate payments beforehand. Avoiding these mistakes can save you a lot of headache and money.

The Role of Regulatory Bodies

Bangladesh Bank is actively trying to tackle the rising problem of loan fraud. They often issue warnings to the public about fraudulent groups that misuse the names of official bodies like the central bank. And the IMF to offer fake loans. It’s a constant battle, honestly. These warnings highlight distinct bogus platforms. And advise people not to share personal information or engage in financial (more than you might think) deals with them. The Payment and Settlement Systems Act, 2024, makes it a serious crime to operate lending platforms without proper, I mean, authorization from Bangladesh Bank, with penalties up to five years in jail or a Tk 50 lakh fine.

The World Bank also issues similar warnings, more exactly stating that they never offer; or rather, loans directly to individuals and never ask for personal or financial information from the public. They've observed fraudsters craft fake Facebook pages. And using mobile banking to collect money by pretending to be the World Bank. Despite these push. Enforcing regulations across the vast digital space is a huge challenge. It’s hard to keep up with every new fake app that pops up, you know? While traditional banking institutions like Meghna Bank and Bank Asia clearly list their interest rates for various loans. Showing transparency, many online loan apps lack this clarity. This makes it really a pain for everyday the majority to tell the awesome from the bad.

Student Loan Landscape: A Distinct Challenge

While, or rather, quite a few students aim for higher education, especially abroad, securing funding all the time puts a heavy burden on families. Around 78% of Bangladeshi students on US campuses are in STEM fields. And a big number fund their education with family sacrifices.

Back in the day, local banks demands a family co-signer. More often than not, this system can limit opportunities for talented students whose families don't own property. Or have high incomes. However, some international private lenders are beginning to offer no-cosigner options. Evaluating a student’s academic program and future earning potential instead. These global lenders can cover broader education costs, including tuition, fees. And living expenses. Which is a major advantage over typical local bank loans that regularly only cover tuition. The processing time for these specialized; I mean, global lenders can also be much faster. Sometimes offering conditional approval in an instant and full disbursement within five days once documents are uploaded. This evolving student loan market suggests a shift. Though slowly, towards more accessible funding models for international studies.

Impact on Personal Finance and Economy

Here's where it gets interesting. The current loan scene, with its mix of rising interest rates. Digital scams. And aggressive recovery practices, clearly affects personal finance in Bangladesh. When people face unexpectedly high interest rates or fall victim to scams. It can lead to massive debt, ruined credit scores, and severe mental stress. The pressure to repay loans with escalating interest from unregulated apps can push individuals into a cycle of borrowing more. In most cases, this build a real financial hole that's tough to climb out of. Take that with a grain of salt, though.

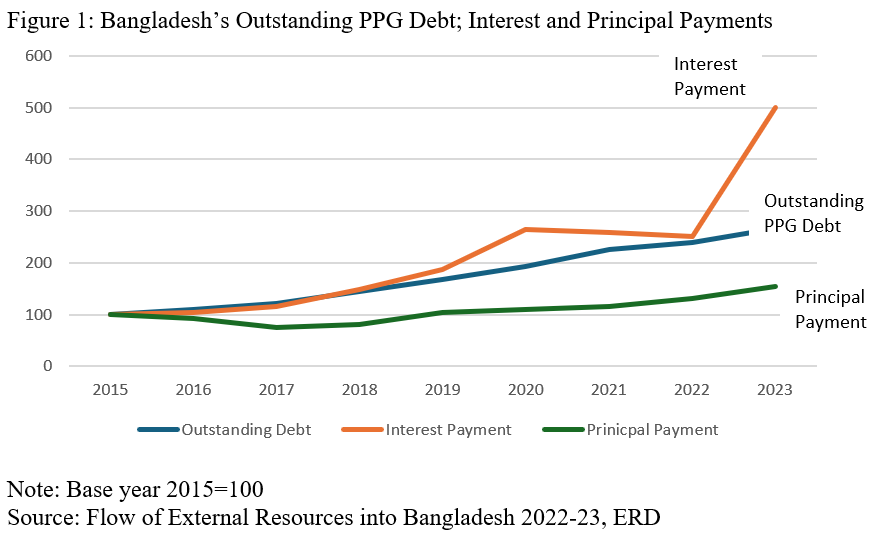

Bottom line on that: blocksep matters. On a broader economic scale, the prevalence of such scams. And high-cost lending can erode trust in digital financial services, slowing down the country's move towards a cashless economy. When private sector credit growth remains sluggish, as it did in November 2025 (below 7% for six consecutive months), it suggests weak investment and can hinder industrial expansion and job creation. Businesses facing high borrowing costs (some banks charging 15-16% interest for entrepreneurs) regularly hesitate to invest, preferring to park funds in government securities offering around 11% returns with minimal risk. Point is, this situation means less money flows into productive sectors, impacting overall economic recovery. Com/bangladeshs-loan-paradox-fast-cash-hidden-traps/) highlights how these issues intertwine.

The Digital Lending Evolution

Digital lending, despite its pitfalls, keeps changing in Bangladesh. Here's the thing; the thing is, the convenience of online loan applications, especially for those in remote areas or without easy access to traditional banks, is undeniable. However, this convenience comes with the make-or-break need for better regulation. And increased consumer awareness. There's a constant tension between accessibility and safety, right? While some online platforms are indeed legitimate. Honestly, the sheer number of fraudulent ones makes it rough for people to distinguish between safe and risky options. This means individuals must become their own best defense.

Believe me, I've been there. The future of online lending will likely takes more stringent regulatory structures to protect consumers, maybe something similar to how non-banking financial companies (NBFCs) are regulated in other countries, making sure more transparency in interest rates and collection practices. Without this, the trust gap will only widen. Com/top-10-profitable-business-in-bangladesh/). Understanding digital lending's risks and rewards becomes even more important.

User Concerns and Social Media Buzz

Social media platforms like Reddit and X are buzzing with user experiences, warnings. And pleas for advice about online loans. People all the time turn to these communities to ask if certain apps are trustworthy or to share their horror stories. This collective sharing craft a key, albeit informal, warning system. Discussions often revolve around the unbelievably high interest rates of some apps. Hidden fees that pop up, and the incredibly aggressive debt collection tactics. " or share experiences of getting "scammed by an online lending scheme I found on Facebook". But hey, that's just my two cents.

These conversations show a deep-seated fear of financial ruin and humiliation. The rapid spread of information on platforms like Reddit, where most of us discuss avoiding payment to fake 7-day loan apps. And the tactics used by collectors, highlights a community trying to find solutions to a pervasive problem. The overall sentiment is one of caution and frustration. Highlighting the need for transparent, fair, and regulated lending options.

Final thoughts

The trends in Bangladesh's loan market. Truth is, particularly with online lending, are pushing individuals toward greater caution. We expect to see continued public awareness campaigns from financial regulators. What's wild is maybe even a dedicated hotline for reporting loan scams. Stricter enforcement of the Payment and Settlement Systems Act, 2024, will become key. Also, traditional banks might start simplifying their digital loan application processes to compete with the speed of online apps. Offering a safer alternative. The demand for clear, low-cost financial products is high, and institutions that prioritize transparency and ethical practices will at the end of the day gain trust and market share. This shift will hopefully lead to a more secure and reliable financial setup for everyone.

FAQs

What are the main types of loan scams happening in Bangladesh?

The main scams involve fake online loan apps. And websites that pretend to be legitimate banks or financial institutions. On average. But demand upfront "processing fees" or "insurance" and illegally collect personal data. Real talk — they constantly misuse logos of Bangladesh Bank and the World Bank to seem real.

How can I spot a fake online loan app or website?

Be cautious of any platform asking for upfront fees. Before disbursing a loan; legitimate lenders usually deduct fees from the loan amount itself. Also, check if the app or website is registered and licensed by Bangladesh Bank. Unregistered apps lack proper oversight, look for unusually high interest rates or vague terms and conditions, which are often red flags.

What happens if I fall behind on payments with an unregulated online loan app?

Unregulated apps might resort to aggressive and unethical debt collection tactics. This can include harassing you. And your contacts using information they collected from your phone. On average, some may send threatening messages, spread false information, or tried to shame you on social media. They might even claim your account is "frozen" and demand more money.

Are student loans readily available for studying abroad from Bangladeshi banks?

Local Bangladeshi banks often provide student loans. But they usually demands a family co-signer or big collateral, like property pledges. However, some global private lenders are emerging, I mean, that focus more on a student's academic program. And potential earnings, offering no-cosigner options for eligible international universities. These options might cover a wider range of education costs, including living expenses. Of course, your mileage may vary.

Why are interest rates so high for some online loans in Bangladesh?

High interest rates on some online loans, sometimes over 20% or even (which makes perfect sense) much higher for unregulated apps. Are often due to the perceived risk of lending to everyone without traditional credit histories or collateral. Another thing, some unregulated lenders operate outside clear legal structures, allowing them to impose exorbitant charges and hidden fees. Not gonna lie, the lack of strong regulation allows these — or rather, apps to charge what the market will bear from desperate borrowers. But then again, it depends.

References / Sources

[1] tbsnews.net