Thinking about using a 401(k) loan to pay off student debt? I’ll give you the short answer: you can borrow from your 401(k), but it often carries big trade-offs that can weaken your retirement savings and create tax or job-risk consequences. If you need quick cash, a 401(k) loan can help now, but it usually hurts your long-term financial health more than it helps.

I’ll walk you through how a 401(k) loan works, when it might make sense, and the safer choices you should weigh first. You’ll get clear facts so you can decide whether tapping retirement money fits your goals—or if refinancing, forgiveness programs, or sticking to your current plan will serve you better.

Key Takeaways

- A 401(k) loan gives fast access to funds but reduces retirement growth.

- Loans can carry tax, penalty, and job-related risks if you can’t repay.

- Consider refinancing, repayment plans, or employer options before borrowing.

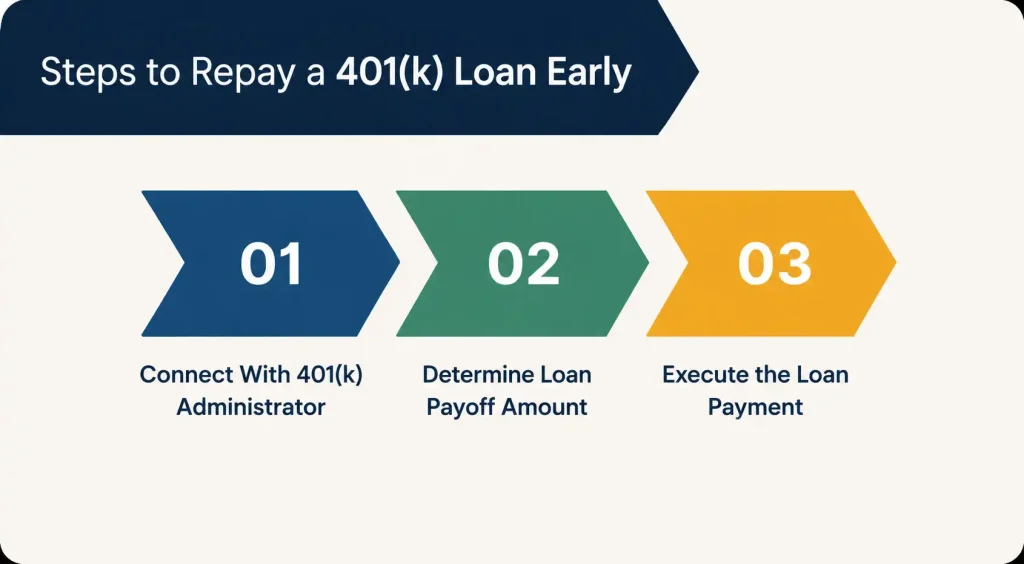

Borrow From Your 401(k)

I can borrow from my 401(k) if my plan allows loans. Many plans let participants take loans up to the lesser of $50,000 or 50% of the vested balance. I must check plan rules and any limits before I apply.

A 401(k) loan avoids the 10% early withdrawal penalty and immediate income tax if I repay on schedule. I usually repay through payroll deductions, which keeps the process simple and automatic.

There are clear risks I watch for. If I leave or lose my job, the loan often becomes due quickly and may count as a taxable distribution if unpaid. That could trigger taxes and penalties, especially if I’m under 59½.

I lose potential investment growth on the money I borrow. Even though I repay myself with interest, the retirement balance can lag behind if the market rises during the loan period. That effect can reduce my long-term savings.

Key points to compare before borrowing:

- Loan amount: Usually up to $50,000 or 50% of vested balance.

- Repayment term: Often 5 years for general loans; longer for home purchase loans.

- Job risk: Leaving the employer can accelerate repayment and cause taxes.

- Opportunity cost: Missing market gains while funds are out of the account.

I weigh these factors against alternatives like income-driven plans, refinancing, or targeted budgeting before I decide.

How 401(k) Loans Work

I explain how borrowing from your 401(k) works, who can take a loan, how you pay it back, and the legal limits on how much you can borrow. Read each part to know the steps, rules, and risks you face if you use this option to pay student loans.

Eligibility Requirements

I must first confirm that my plan allows loans. Not every 401(k) plan permits loans; plan documents or the plan administrator tell you if loans are allowed.

I must be an active participant in the plan. Employers generally require you to be an employee and to have a vested balance before you can borrow. Vested means the portion of your account you own outright.

I also need to meet any plan-specific rules. Plans sometimes set minimum service time, require loan applications, or limit the number of active loans. If you work for a company that recently adopted SECURE 2.0 features, check whether they added a student-loan match separate from loan rules.

Repayment Terms

I repay 401(k) loans with after-tax dollars through payroll deductions in most plans. The standard maximum term for a general-purpose loan is five years. Shorter terms may apply if the loan is for a primary residence.

I pay both principal and interest to my own account. The interest rate is typically tied to the prime rate plus a margin, but the plan sets the exact rate. If I leave my job, the loan may become due quickly—often within 60 to 90 days—or the outstanding balance may be treated as a taxable distribution.

I must also consider missed payments. Late or missed payments can trigger plan rules that convert the balance to a distribution, which can create income tax and a 10% early withdrawal penalty if I’m under 59½.

Borrowing Limits

I can generally borrow the lesser of 50% of my vested account balance or $50,000. The $50,000 cap applies after reducing outstanding loan balances; for example, if I already owe $10,000, the cap may reduce the new loan amount to $40,000.

Plans may impose lower limits than federal rules. Some plans set per-loan minimums or maximums, or they prohibit concurrent loans. If my vested balance is small, the 50% rule can severely limit borrowing.

I should also remember that borrowing reduces the amount invested and can hurt long-term retirement growth. Even though I repay myself with interest, missing market gains while money is out of the account is a real cost to consider.

Evaluating 401(k) Loans Versus Student Loan Repayment

I compare the real costs, retirement impact, and credit effects so you can weigh taking a 401(k) loan against keeping student loans. Below I cover how interest, savings loss, and credit score changes usually play out.

Interest Rate Comparisons

I look at the numbers you pay and the money you forgo. A 401(k) loan typically charges a fixed rate tied to prime plus a small margin, often 1–2% above market. You repay that interest to your own account, but the real comparison must include after-tax effects and lost investment growth on the borrowed amount.

Student loans come in varied rates: federal loans can be 0–8% depending on program and consolidation, while private loans often run higher. If your student loan rate is lower than the 401(k) loan effective cost (including lost returns), keeping the loan usually makes more sense. If you can refinance student debt to a much lower rate or have a high-rate private loan, a 401(k) loan can look attractive short term — but you must factor in timing, tax treatment, and job risk.

Impact on Retirement Savings

I treat retirement balance loss as a long-term cost, not just a temporary gap. With a 401(k) loan, the principal leaves your invested balance and stops compounding. Even if you repay interest to yourself, the loan interrupts market returns and possible employer matching on future contributions.

If you withdraw early or default on the loan due to job loss, the outstanding balance becomes taxable and may incur a 10% penalty if you’re under 59½. That can dramatically increase the cost. I recommend running a projection: estimate expected market return lost over the loan period and compare it to the student loan interest saved. That gives a clearer picture of the retirement hit.

Credit Score Considerations

I focus on how each option affects your credit file. A 401(k) loan does not require a credit check and does not appear on your credit report. That means it won’t directly lower your credit score or affect your debt-to-income ratio for mortgages or other loans.

Student loan repayment, consolidation, or refinancing does show on credit reports. Making on-time payments can build your score, while missed payments hurt it substantially. Refinancing may require a credit pull and could change your credit mix. If maintaining or improving credit matters for an upcoming mortgage or rental, keeping and managing the student loan may offer benefits a 401(k) loan cannot provide.

Potential Benefits of Using Retirement Funds for Education Debt

I see a few situations where tapping retirement funds can help. The main gains are simpler debt handling and a smaller monthly cash outflow.

Simplifying Debt Management

I can use a 401(k) loan to combine multiple student balances into one payment. That cuts the number of creditors I deal with and makes tracking due dates easier. Many 401(k) plans let me borrow up to 50% of my vested balance or $50,000, whichever is less, so I can cover a large portion of loan principal in one move.

A single loan often has a fixed repayment schedule, so I know exactly when the loan will be paid off. I also pay interest to my own account instead of a bank, which can feel like keeping money in the household. I must watch plan rules and repayment terms, though, because job changes can accelerate repayment or trigger taxes and penalties.

Reducing Monthly Payments

Taking a 401(k) loan can cut my monthly cash payments if the loan term and amount lower my required outflow compared with existing student loan payments. This can free cash for rent, an emergency fund, or other high-priority bills.

I should compare the loan’s monthly payment to my current student loan payment and factor in taxes, penalties, and interest lost from investments. Remember, while payments to a 401(k) loan may look lower, I stop earning compound returns on the borrowed amount until I repay it. If my job is unstable, the risk of having to repay the loan quickly could raise my monthly burden.

Risks and Drawbacks to Borrowing From Your 401(k)

I will point out the biggest downsides you face when you tap your retirement plan to pay student loans. Expect tax issues, possible penalties, and serious risks if your job changes.

Tax Consequences

If you treat the money as a loan and repay on schedule, you usually avoid immediate taxes.

But if the loan is treated as a distribution — for example, because you miss payments or leave your job — the outstanding balance becomes taxable income in that year. That can push you into a higher tax bracket and raise your federal and state tax bills.

Also, if you repay the loan with after‑tax dollars, you pay taxes again on that same money when you withdraw it in retirement.

This creates a double‑tax effect on the portion you repaid with after‑tax income, reducing the long‑term value of the funds you used.

Early Withdrawal Penalties

Taking money out of a 401(k) before age 59½ can trigger a 10% early withdrawal penalty if the distribution is not a qualified loan or otherwise exempt.

If a loan converts to a distribution, you face both the penalty and ordinary income tax on the full unpaid balance.

There are limited exceptions to the 10% penalty, and student‑loan use generally does not qualify.

That means using 401(k) funds for student loans risks unexpected fines if anything goes wrong with the loan status.

Employment Termination Impact

Most plans require loan repayment within a short window if you leave your job.

If you are laid off, fired, or quit, the unpaid loan balance often becomes due immediately or within months.

Failure to repay triggers a deemed distribution, so the unpaid amount becomes taxable income and may incur the 10% penalty.

This can create a large, sudden tax bill at a time when income is already reduced.

Leaving a job also cuts off future employer matching while you work to repay the loan.

Reduced contributions and lost matches shrink your retirement saving power and compound the long‑term cost of borrowing.

Alternatives to Leveraging 401(k) Assets for Student Loan Repayment

I’ll outline practical options that can lower monthly payments, reduce interest costs, or provide employer help so you don’t tap retirement savings. Each choice has trade-offs around fees, taxes, and long-term cost.

Refinancing and Consolidation

Refinancing replaces one or more student loans with a new private loan, often at a lower interest rate if you have good credit and steady income. I check current rates, fees, and whether the new loan is fixed or variable before I apply. Refinancing federal loans into private loans removes federal protections like income-driven plans and forgiveness, so I avoid refinancing if I need those benefits.

Consolidation (federal Direct Consolidation) combines federal loans into one loan and can simplify payments. I use consolidation mainly to access alternative repayment plans or to restart progress toward forgiveness programs, but it may increase total interest paid. I compare lenders, run prequalified rate checks, and read terms so I know the true monthly savings and total cost.

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans set monthly federal loan payments based on income and family size, often lowering payments to 10–20% of discretionary income. I gather my recent tax return and pay stubs to estimate eligibility and monthly amounts. IDR plans can offer forgiveness after 20–25 years of qualifying payments, but forgiven balances may be taxable depending on the law.

I recertify income each year; missing recertification can raise payments or undo progress. For public servants, I look into Public Service Loan Forgiveness (PSLF) where payments under IDR can count toward forgiveness after 10 years of qualifying work and payments. I weigh lower monthly cost now against longer repayment timelines and potential tax implications later.

Personal Loans

A personal loan can pay off student loans if I qualify for a lower rate than my current loans. These loans usually have fixed terms and predictable monthly payments, and they won’t affect retirement accounts. I compare annual percentage rates (APR), origination fees, and prepayment penalties across banks, credit unions, and online lenders.

Using a personal loan for student debt removes federal borrower protections, so I avoid this if I need income-based relief or loan forgiveness. I run the numbers: total interest paid, monthly payment, and how the new loan fits my emergency savings. If I have strong credit, a personal loan can simplify finances and lower interest; if not, it may cost more than keeping the student loans.