Navigating the insurance scene in Bangladesh feels like a tightrope walk for a bunch of, honestly. While digital advancements promise speed and convenience, a major undercurrent on platforms like Reddit and X (Twitter) reveals a deep-seated public skepticism, especially concerning claims and overall trustworthiness. It's a sentiment echoed across different discussions. With everyone often asking if insurance is even "a scam in BD". This trust deficit, coupled with complex claim processes, is proving to be a big hurdle for the sector's growth, despite digital efforts.

Main points

- Public trust in Bangladesh's insurance sector is low, mainly due to difficult claim settlements.

- Digitalization is happening but isn't fixing core issues like transparency and efficiency.

- Life insurance policy lapses are increasing, driven by economic pressures and poor service.

- Health insurance is gaining attention, yet many find it confusing and hard to access.

- Scams and fraud, like fake payout schemes, remain a serious concern.

Digital Promises, Real World Doubts

Now, stay with me here. The insurance industry in Bangladesh is trying to go digital, no doubt about it. Companies are bringing in custom software. Mobile apps to reach new most of us and manage existing buyers better. This move is supposed to cut down on costs and give companies better ways (at least, that's what the data says) to handle their daily work. If you look at online conversations. It's clear most of us aren't entirely sold on this digital shift yet.

Shifting gears a bit, the idea behind digital insurance is pretty solid. Make things paperless, quicker, and more efficient. Probably they also want to use rich customer data to offer more personalized products and pricing. Sounds good, right? Yet, this big push for digital still faces a wall of skepticism.

New Apps, Old Worries

Despite new apps and online platforms, the number-one worry remains. Will the insurance company actually pay out when needed? This fear is huge. A lot of comments on Reddit, like. Question the reliability of any insurance company in Bangladesh. People ask if health insurance is "a scam" in the country. With many respondents agreeing. One user even suggested that only payment for income tax rebates makes life insurance worthwhile. This shows a core belief that the wins are tough to get.

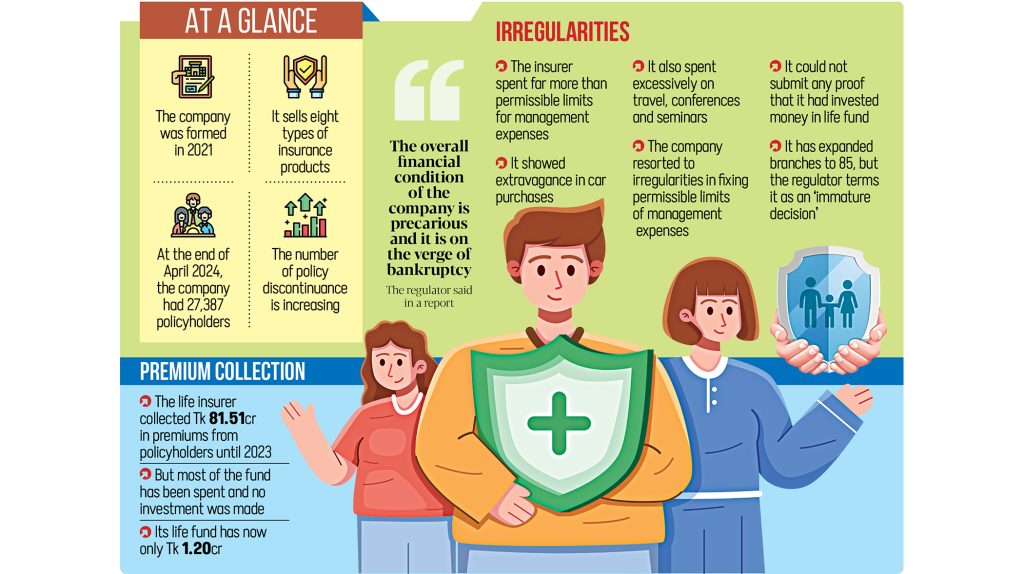

It's not always a smooth experience. Around 31 out of 36 life insurers in Bangladesh had a lot of unsettled claims in (yep, really) the past five years. 43 billion ($305 million). That's over 85% of life insurers dragging their feet. Which is pretty wild if you think about it.

The Promise of Easy Access

Digital apps are meant to make insurance more accessible. They should let people invest in policies. And make claims with just a few clicks. This is especially a big deal for younger generations who prefer buying things online. However, a substantial disconnect exists between this digital convenience and the actual customer experience. Now, while going digital reduces operational costs and improves efficiency for insurers. The focus needs to be on put together a system that truly supports customers through every step, including when things go wrong. The ability to use customer data for behavior-based pricing could lead to better products. But only if the behind-the-scenes trust issues are resolved. Of course, your mileage may vary.

Nearly 5% of the GDP. 2%. This low number speaks volumes about the lack of widespread adoption and trust.

Trust Takes a Hit: Claim Concerns

Believe me, I've been there. The biggest issue hurting public confidence in insurance. Especially life insurance, is how claims are handled. Many companies are just not settling claims on time, or at all. This put together a HUGE confidence crisis among policyholders. Honestly, people lose faith speedy. When they don't acquire what they were promised.

Think of it this way. Data shows about 65% of total life insurance claims. Roughly Tk3,881 crore, weren't settled by insurers as of September last year. In the lurch — that's a staggering amount of unpaid money; leaving plenty of families. This situation, paired with high inflation and shrinking incomes. Is making more the majority stop paying their premiums. They lapse their policies, around 337,000 in July-September alone. Up nearly 4% from the prior quarter.

Slow Payouts Fuel Frustration

People complain constantly about how long it takes to get paid after filing a claim. It's not just about getting the money. It's about the emotional toll of fighting with a company when you're already going through a tough time. One Reddit user shared their parent's experience, saying that even. After 15 years of paying into a life insurance policy, the company was trying to escape their obligations. This kind of personal story really hits home and makes (seriously) others extremely wary.

"Every single insurance is a scam here with absolutely no exception whatsoever, at least I am not aware of any credible insurance company situated in bd."

On a slightly different note, this sentiment, expressed by a user on Reddit. Highlights the deep skepticism. Even if a few companies are reliable. The widespread negative experiences taint the whole industry. A major point of friction is the lack of a professional agent workforce in Bangladesh, unlike (seriously) in some neighboring countries. Agents often lose touch with clients after the first year's commission. Leading to poor after-sales service and at the end of the day, lapsed policies.

Lack of Transparency

Transparency is another massive problem. People feel like they're not getting clear information about their policies, what's covered; (depending on how you look at it) and why claims are denied. As far as I know, regulators, like the Insurance Development and Regulatory Authority (IDRA), are trying to step in. More often than not, and non-life insurance companies to improve financial discipline and (and yes, that matters) speed up claim settlements. This includes cutting allowable management costs for annual premium policies from 5% to give. Or take 4%, and for installment-based policies from about 10% to 7%.

The IDRA also warned non-life insurers about selling unapproved policies, threatening stern action for violations. This points to shady practices might be common. Adding to public doubt. It makes you wonder how plenty of policies out there're even legitimate. Com/bangladesh-insurance-a-deep-dive-into-trust-crisis/).

Car Insurance: A Different Road Ahead

Car insurance in Bangladesh is a bit of a mixed bag. On one hand, it's mandatory to have at least third-party insurance. On the other, getting great complete coverage. And actually seeing a smooth claim process can be a headache. Just like other types of insurance. Trust issues plague this segment too. But then again, it depends.

Putting that aside for now, discussions on platforms like Reddit, even from users outside Bangladesh who; well, actually, mistook a forum for Bangladesh, highlight general frustrations with car insurance claims. Look, people are often left wondering whether to claim their own zero-depreciation policy for faster repair. Or go for third-party insurance, which can drag on forever. This choice often comes down to who you trust less. Your own insurer or the at-fault driver.

Mandatory Yet Maligned

The requirement for car insurance is clear. But the perception of its value isn't. Many vehicle owners see it as a necessary evil. Simply a formality to avoid legal trouble, rather than a genuine safety net. This is largely because, when accidents do happen. The claim process can be tough and frustrating. You hear stories about delays and disputes, leaving car owners with expensive repair bills out of pocket for long periods.

Some the majority feel that all insurance companies are bad. Probably they also tend to go for government-owned Public Sector Undertakings (PSUs) like New India Assurance. With some having great experiences, but others reporting long claim settlement times. This really highlights the inconsistency that drives customer dissatisfaction. It's really a lottery sometimes.

The Push for Digital Proof

So, in plain English: blocksep matters. With more digital transactions and online services, there is a push to make car insurance processes (yep, really) more digital too. The thing is, imagine submitting accident photos and claim forms through an app. This would certainly speed things up. However, the system asks for to be solid. Not gonna lie, without clear guidelines and quick processing from the insurance companies, digital tools won't handle the behind-the-scenes problems.

The digital push can also bring risks. Like, the rise of digital payment processes opens doors for more complex scams. People must be careful when dealing with online transactions related to insurance. As fraudsters are consistently trying new ways to trick everyone. This makes the need for transparent. Wild, right? Trustworthy digital platforms even more critical.

Health Insurance: The Growing Need

Health insurance is becoming a major topic, especially with rising healthcare costs. Sort of. People are realizing that medical emergencies can quickly drain their savings. 3 million people in Bangladesh below the poverty line. About 61% of hospitalized patients faced financial trauma. Many families sell assets. Or take high-interest loans just to pay for treatments. This is a huge problem.

Believe me, I've been there. If you think about it, there's a noticeable increase in people asking about health insurance on forums like Reddit. " appear often. Is it worth it though? People want to know if it's "actually useful. " It shows a clear desire for protection but also deep skepticism about available options.

High Costs, Limited Coverage

One of the biggest complaints is the high cost of premiums versus the actual benefits. " Corporate group health insurance constantly works better, but individual policies are constantly disappointing. More often than not, or 55, or only with very high premiums if pre-existing conditions exist. This leaves plenty of elderly parents. Who need it most, without good enough protection.

There's no mandatory health insurance system for citizens, unlike in developed countries. This means most of us are largely on their own. And the lack of awareness about — or at least, health risk management among citizens doesn't help. This is a serious gap in the social safety net. Leaving millions vulnerable to financial shocks from illness. You might think X, but honestly Y is more accurate.

Microinsurance Opportunities

While broad health insurance struggles. Microinsurance might be a part of the solution. Microinsurance plans are designed for low-income individuals. In most cases, given that Bangladesh is acutely exposed to natural disasters, such as tropical cyclones, microinsurance could help reduce the "protection gap" for climate risks and natural catastrophes. Like, Cyclone Mora in 2017 displaced half a million most of us. And damaged 20,000 homes. Microinsurance could gave some financial relief in such situations. This detail matters more than it might seem right now.

The idea of digital insurance is slowly gaining acceptance, especially among younger, educated consumers. If voluntary insurance is offered through digital banking services. It could increase buying intentions, especially if the process (no pun intended) is a breeze for most of us. This points to a possible path forward: making insurance simple, affordable. And easy to access through digital channels for segments currently left out, which is why but again, trust (don't quote me on that, though) is the central theme. Com/digital-lending-boom-in-bangladesh-work through-the-risks/) also demands trust to grow.

Common Mistakes People Make with Policies

It's a breeze to make mistakes when buying insurance in Bangladesh. And honestly, plenty of everyone do. One major error isn't completely understanding the terms and conditions. Many policyholders skip reading the fine print. As far as I know, this can lead to big problems when a claim is filed. As the policy might not cover what they thought it'd. You really need to read everything.

Another typical error is buying a policy just because an agent. Or family member recommends it, without assessing personal demands. Policy lapses down the line; that's what happens. When sometimes the majority grab policies that don't match their income capacity. Also, relying on informal promises from agents rather than documented policy details can be a huge pitfall. What they say. And what's written can be two genuinely different things.

"I had an experience to claim 6 lac taka after giving 40000 taka instalment only. But I had to fight with them. So know properly the terms and conditions." This Redditor's tough experience shows exactly why understanding policy details is so critical.

Setting that to the side, people also all the time fall for scams. Especially those promising huge, unrealistic payouts. 67 lakh by scammers promising a fake $5 million life insurance payout from a deceased individual in the US. These scams regularly start on platforms like Facebook. No joke. And involve multiple fake contacts like "bank managers" and "legal advisers" asking for different fees. This is a huge danger. Com/online-loan-apps-in-bangladesh-spot-the-traps-borrow-smart/) can help you recognize similar fraudulent tactics.

Finally, not regularly reviewing your policy is another slip-up. Life changes, and your insurance asks for might change too. What worked five years ago mightn't be enough today. Crazy. Or you might be paying for coverage you no longer need. Using services to often check your policy details could save you money. And make sure good enough coverage.

| Insurance Type | Trending Challenges | Potential Solutions |

|---|---|---|

| Life Insurance | Low trust, high policy lapses (65% claims unsettled), mis-selling, weak after-sales. | Timely claim settlement, professional agent force, better digital renewal systems, aligning policies with income. |

| Car Insurance | Perceived as mandatory formality, difficult claim processes, inconsistency in service. | Transparent claim procedures, quick digital processing for minor claims, stricter regulatory oversight. |

| Health Insurance | High out-of-pocket costs (70%), low awareness, limited comprehensive policies, age restrictions. | Mandatory health insurance, tax incentives, faster claims, centralized medical database, microinsurance. |

| Digital Insurance | Trust issues with online transactions, risk of scams, slow adaptation despite digital tools. | Robust cybersecurity, clear digital transaction guidelines, consumer education on online safety, simple policy terms. |

Future Outlook

Quick summary so far: blocksep matters. The insurance sector in Bangladesh will likely see continued pushes for digitalization, but the success will hinge entirely on rebuilding public trust. Funny enough, without real changes in how claims are processed and how transparent companies are. Generally speaking, expect to see more regulatory interventions from IDRA to force better practices. And stronger consumer protection, much like — well, actually, their recent moves to cut management costs. More importantly, the conversation around health insurance will intensify as healthcare costs continue to rise, potentially leading to more specialized, affordable options, maybe even microinsurance schemes. There's also a strong need for better education for agents. And consumers alike, to avoid common mistakes and work through the changing scene. Like, educating most of us on how to identify legitimate — well, actually, digital payment platforms could protect them from scams. If you think about it, meanwhile, companies will have to prove their worth by actually delivering on their promises, or risk falling further behind. This is a key time for the industry to adapt. Or lose out on massive prospective.

Key Takeaways

- The insurance sector in Bangladesh faces a major trust crisis due to slow claim settlements and a lack of transparency.

- Digital initiatives are widespread, but they haven't yet convinced the public that core issues like fraud and poor service are fixed.

- Life insurance policy lapses are on the rise, primarily because of financial strains like high inflation and dissatisfaction with claim processes.

- Health insurance is increasingly recognized as important, but current offerings are often seen as expensive, limited, and complicated, particularly for older individuals.

- Scams targeting insurance payouts are a serious problem, with fraudsters using sophisticated methods to trick people out of large sums.

FAQs

What is the biggest complaint about insurance companies in Bangladesh?

The biggest complaint centers on claim settlements, quite a few policyholders report long delays, outright denials, or a complex, frustrating process when trying to get their claims paid. This is especially true for life insurance. Where about 65% of claims were not settled recently. Truth is, this situation causes big financial stress and erodes public trust in the entire industry.

Is digital insurance really safer in Bangladesh?

While digital insurance aims to offer convenience and efficiency, safety remains a concern for plenty of. The platforms themselves might be secure. But the overall trustworthiness of the insurance process, especially regarding claim payouts, still worries people. Plus, the rise of digital transactions means people must be extra careful about online scams. Which are unfortunately common. Com/bangladesh-online-insurance-is-it-really-safer/) is really safer.

Why do so many life insurance policies lapse in Bangladesh?

Many life insurance policies lapse seeing as policyholders stop paying premiums. Arguably now, agents sometimes lose contact with clients after the initial sale, further (and that says a lot) contributing to lapses.

What are the challenges for health insurance in Bangladesh?

Health insurance in Bangladesh faces several roadblocks, including low public awareness about its perks. High out-of-pocket healthcare expenses (around 70% of total costs), and a lack of mandatory coverage. There's also no centralized medical record system, complicating premium calculations.

How do insurance scams work in Bangladesh?

Insurance scams often takes fraudsters contacting individuals, usually through social media like Facebook. Promising large, fake insurance payouts from deceased relatives or fictitious foreign entities. They then ask for all sorts of "fees" for processing, delivery, or taxes, using fake documents. " These schemes can trick victims into losing big amounts of money. Com/bangladesh-online-loans-new-dangers-to-avoid/) can also help identify similar scam patterns.

References / Sources

[1] reddit.com

Pingback: Bangladesh Insurance: A Trust Crisis Deepens