Bangladesh's insurance world is facing a deep trust crisis. Honestly, it's making people insanely skeptical. You probably know people who've dealt with insurance companies. Found it complicated, maybe even frustrating. ) for things to go wrong. It's a big deal. Because insurance is supposed to protect you, not cause more headaches. This blend of established trust issues and new digital worries is exactly what's buzzing across social media and financial discussions right now. " but the sheer volume of complaints. The regulatory responses make this moment different.

Trust Issues and Digital Risks Explode

The biggest trend is a growing distrust in Bangladesh's insurance sector, with tons of policyholders feeling cheated, especially as (don't quote me on that, though) digital services become more common. You'll want to remember this for what's coming next.

Honestly, it feels like everyone's talking about the, well, actually, insurance (no joke) sector in Bangladesh right now. And not for impressive reasons. There's a real buzz on places like Reddit and even in the news about how people just don't trust insurance companies. " That's a strong statement. And it points to deep unhappiness. A particular Reddit thread in February 2025 asked if health insurance in Bangladesh was a scam, and a lot of comments said yes, outright. " This level of public frustration is something you can't ignore. Or at least that's how it seems.

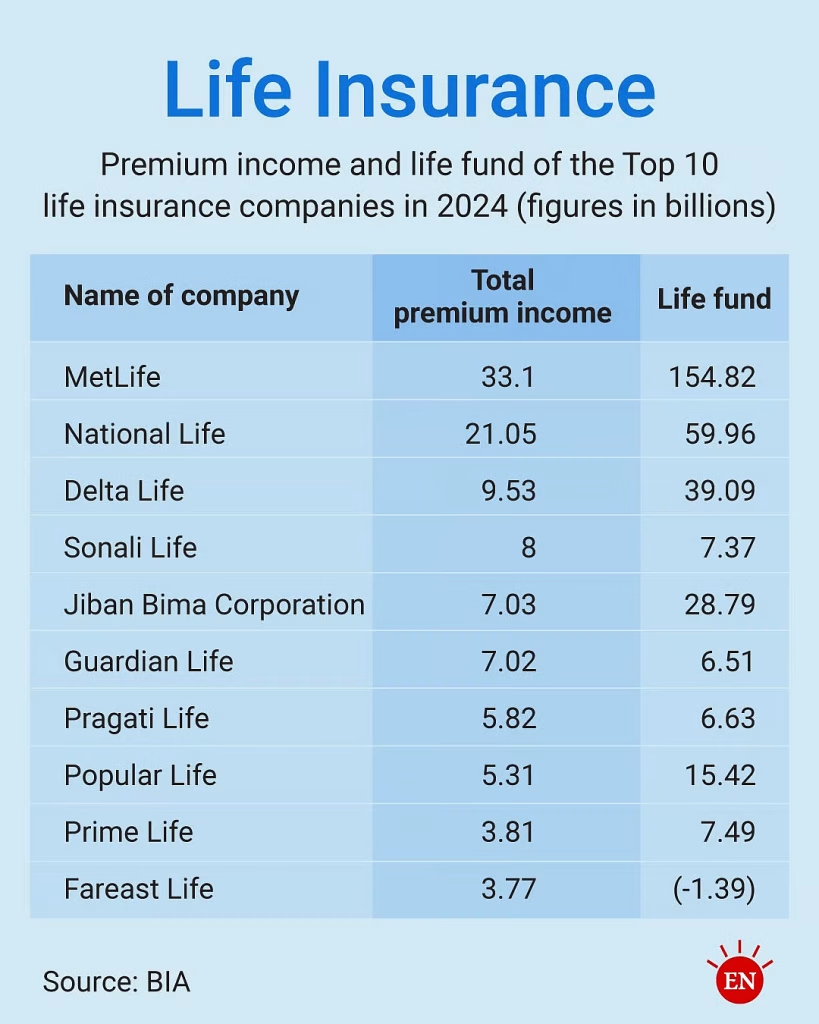

The numbers don't lie, either, and back in 2023, the Insurance Development and Regulatory Authority (IDRA); well, actually, saw a massive 24,605 complaints against just 14 life insurance companies in the first ten months alone. Get this: only about 14% of those claims were settled. That's pretty low. Most of these complaints, about 95% of them. Were about companies not paying out claims when policies matured. Other issues included bad investments and outright fund embezzlement. The Anti-Corruption Commission has even sued people, including bank officials, for allegedly embezzling over Tk11 crore from insurance companies, which is quite a fair (no joke) number of money. These kinds of stories spread rapid, shaking confidence in the whole system. 1 million policyholders (and it actually works) can't get their dues. A problem made worse by firms that supposedly embezzled Tk3,736 crore. But then again, it depends.

At least 57% in 2018. The reasons? In many cases, it's like a repeating cycle, only now digital platforms are making it all more visible.

Where Digitalization Intersects with Trust

You'd think going digital would make things better, right? More transparency, easier access. But it’s a mixed bag. The push for online insurance is real. With IDRA trying to get all private companies onto digital platforms. The idea is to make buying insurance faster. And easier, especially for younger people who do everything online. Some experts even say bancassurance, where banks sell insurance. Can help seeing as people already trust banks more. That makes sense.

Here's the kicker. Digital platforms also build new ways for scams and problems to happen. Scammers are now incredibly sophisticated, posing as agents and using personal details to trick people. They might call you with urgent messages about missed updates. Or lapsed policies, even claiming to have spoken to your family. As it turns out, one person was swindled out of Tk17 lakh in a fake life insurance scam involving a fictitious $5 million payout. It involved Facebook messages, WhatsApp, and fake customs officials. This is really, really worrying.

| Aspect of Trend | Traditional Concerns | Digital Era Concerns | Impact on Trust |

|---|---|---|---|

| Claim Settlement | Delays, excuses, lack of transparency | Digital loopholes, online claim refusal | Lowers public confidence in payouts |

| Fraud | Agent mis-selling, internal embezzlement | Online impersonation, phishing, fake portals | Creates intense skepticism and financial loss |

| Product Access | Limited options, agent dependency | Misleading digital pitches, data privacy | Fuels doubt about policy suitability |

| Awareness | Low general understanding | Information overload, identifying real vs. fake | Confuses consumers, makes them vulnerable |

| Regulation | Weak enforcement, slow response | Difficulty policing online spaces | Shows a gap in consumer protection |

This table clearly suggests the shift. While old problems persist, new digital threats are adding layers of complexity, making the task of building trust harder.

Why This Matters So Much to You

In tons of cases, point is, affects you directly, whether you're looking for life, health, or car insurance. Think about it: life insurance is supposed to protect your family after you're gone. Health insurance helps with medical bills. Car insurance keeps you safe on the road. If you can't rely on these, then what's the point of paying premiums? It undermines the very idea of financial security.

The takeaway is simple: blocksep matters. Loads of the majority in Bangladesh skip insurance, or at least, altogether, not mainly because they don't see the need. But because they don't believe it'll actually help them when they need it most. Around 90-94% of the poor are without micro-insurance coverage, despite a large market; this means millions are left exposed to financial shocks from illness or death. Some policyholders even believe insurance is restricted in Islam. Truth is, which is actually not true, but this belief acts as a barrier. Honestly, this skepticism is understandable when you hear stories about policies not paying out. Com/decoding-bangladeshs-loan-app-craze/) too. And the feeling of uncertainty is much the same.

"When fraudulent activities go unpunished, this trust collapses. Honest customers bear the burden of inflated premiums, while genuine claimants face delay and denial."

If you're paying your premiums on time? But if companies are slow to pay. Or even worse, if they've embezzled funds, it hurts everyone. This is not just a small inconvenience; it's a breakdown in a fundamental financial tool that should shield you from disaster.

Common Mistakes People Make

One big mistake the majority all the time make is focusing only on the lowest premium without really digging into the terms and conditions. For the most part, another big error is trusting agents too easily without verifying their identity. Or checking company legitimacy. Scammers often have just enough personal info to sound convincing. You need to verify who you're talking to. A third mistake isn't knowing how to complain or follow up effectively when a problem; or at least, arises, and a bunch of folks in rural areas, like, don't even know how to file a complaint.

" This is pretty rough, if you think about it. It’s supposed to be peace of mind, not more stress.

Think about that. The future of insurance in Bangladesh, honestly. Hangs on how the industry tackles this trust; I mean, deficit head-on, especially as digital services become more common. Regulators are trying to step up. Plus — the IDRA — like, is planning a new "Insurance Resolution Ordinance" to help recover embezzled funds and restructure troubled companies. This could even let them sell off assets of directors involved in fraud. Which is a pretty powerful move. Though results vary.

The idea is that banks already have customer trust, so they can assist boost insurance penetration. It means you might buy life insurance. Or health coverage right through your banking app, which sounds convenient, right? This move could assist people manage savings, payments, and loans all in one place, the government's National Financial Inclusion Strategy (NFIS) 2021-2026 even aims to introduce bancassurance and fresh products for ordinary people.

However, for bancassurance to actually work. It has to deliver real value. If claims processing remains slow or unclear, it could hurt both the insurer and the bank; strong data privacy rules and clear customer consent will be really key here. It’s a delicate dance between making things a breeze. And keeping them secure.

What's Changing for Different Insurance Types?

-

Life Insurance: The focus is on making it simpler and more trustworthy. With more than 85% of life insurers having outstanding claims, the pressure is on. New, flexible, and lifestyle-linked products are emerging, especially for younger people who want benefits they can use for life events, health, or wellness. This moves life insurance from just a death benefit to something more active and useful. It's a smart change, if they can deliver. You might be interested in how the broader Bangladesh insurance trust crisis deepens and what that means for different policy types.

-

Health Insurance: This area faces huge skepticism. Only about 0.4% of the population has health insurance. People often find it cheaper to pay out of pocket. The lack of digital infrastructure and centralized medical records is a big problem. But there's a push for universal health coverage by 2032. This would require significant investment in digital health systems and awareness campaigns. Honestly, it will take some serious work to convince people it's not a scam.

-

Car Insurance: The market is seeing changes too. Motor insurance actually accounts for the largest number of policies from a single type of general insurance in Bangladesh. A new law was even proposed to make motor insurance compulsory for all registered vehicles. This is a big shift, especially since third-party insurance became non-mandatory under the Road Transport Act 2018. Premiums are changing, not just based on car value, but also on rising repair costs for parts and labor. So, even if your car gets older, your premium might go up. You gotta check with different companies before renewing.

Avoiding Common Pitfalls

To truly protect yourself in this evolving scene, you need to be smart. First, always verify. Mind you, if someone calls you about your policy, even if they've some details, hang up and call the official company number yourself. Don't trust links sent via text or WhatsApp for sensitive info. Believe it or not, these fake insurance agent scams are becoming incredibly convincing. Second, read the fine print. Seriously, read every word of your policy. Many life insurers restrict health perks after a certain age, like 50 or 55, or (and it actually works) won't cover certain illnesses. Knowing these details can save you a lot of grief later. Third, compare policies. Don't just stick with your current provider out of habit, especially for car insurance. Premiums can vary a lot, and checking with other companies (at least in my experience) could save you money. About 7 out of 10 the majority who shop around, well, actually, find better deals, or at least that's how it seems. Com/bangladesh-online-insurance-is-it-really-safer/). Always double-check the legitimacy of the platform.

Setting that to the side, remember, the goal of insurance is protection, not confusion. Plus, if a deal sounds too impressive to be true, it probably is. And if you feel pressured, take a step back. There's no rush for your financial security.

Key Takeaways

- Trust is critical: A major lack of trust impacts insurance uptake in Bangladesh.

- Digital brings new risks: Online scams, impersonation, and data privacy concerns are growing.

- Regulations are changing: IDRA is trying new laws to combat fraud and protect policyholders.

- Bancassurance rising: Selling insurance through banks could build confidence and reach more people.

- Consumer awareness is low: Many don't understand policies or how to file complaints effectively.

- Verify everything: Always confirm agent identity and policy details directly with the company.

- Read policy documents closely: Understand exclusions and terms, especially for age or pre-existing conditions.

- Shop around for best rates: Don't assume your current premium is the only option, particularly for car insurance.

Questions You Might Have

How common are insurance scams in Bangladesh right now?

Honestly, insurance scams are pretty common and they're getting more clever. Scammers impersonate agents, use social media like Facebook and WhatsApp to trick the majority, and regularly have personal information to make their stories sound real. They might ask for OTPs. Or bank details under false pretenses.

What's "bancassurance" and how might it help?

Bancassurance means banks sell insurance items through their network and digital channels. The hope is that seeing as most of us constantly trust banks more than insurance companies. This model can make insurance seem more reliable and easier to get. It could also make buying and managing policies more smooth, right from your banking app.

Branching off from that, it might seem weird, but car insurance premiums are going up not just because of your car's value. But also because the cost of parts and labor for repairs keeps rising every year. Point is, even if your car depreciates, the overall cost to fix it's increased, so insurers pass that cost on. Believe it or not, you should pretty much always check quotes from different companies before renewing.

Is it hard to make a health insurance claim in Bangladesh?

Here's where it gets interesting. Many the majority report that making health insurance claims can be tough, with some saying they had to "fight with them" to get their advantages. Done. Hospitals might make you pay first. And then claim reimbursement later, which can be a hassle. Also, some policies have age restrictions, like not covering a bunch of illnesses after age 50-55.

What's the main challenge for micro-insurance in Bangladesh?

Micro-insurance, which helps low-income most of us, faces hurdles seeing as loads of potential clients don't fully understand insurance (if you're into that sort of thing) as a risk-management tool. They all the time see premiums as just an expense rather than an investment, so there's also a big lack of trust in providers, making it tough to increase coverage.

What should I do if I suspect an insurance agent is fake?

If an agent calls you and asks for personal details. On average, then, call the insurance company's official customer service number; I mean, directly to verify the agent's identity and the information they shared. Never share OTPs or account numbers with unverified callers. That's a huge tip.

Final Thoughts

The insurance scene in Bangladesh is clearly at a turning point. The industry's future success depends on rebuilding shattered trust — adapting to new digital realities; and cracking down (which is completely normal) rough on fraud. Period. This will need more than just new laws. It needs a real change in how companies deal with customers. Expect to see more digital options, but be extra careful. The push for workarounds like bancassurance could make insurance more accessible. Arguably until then, you need to be your own best advocate, staying informed and asking tough questions to protect your money and your future.

## References / Sources

[1] [reddit.com](https://vertexaisearch.cloud.google.com/grounding-api-redirect/AUZIYQEKJyoqMELmMcqvvqpc1-9a3vxdZJbK1gSOHk5gS8nvz5aXPkK5nlMWJ2K2tubHrDHXPiEB4GuoqDDtNQHqaheDXdsKfvjEN00vcB7T1Z9_d3e511leJHpT9PO7fpj_HLsJzYDhLA9Sm52HxcwLNC0IXGo6GqFeThJkMlYHNcbRdio-TwDww-jF9V3D7A==)