Key Takeaways

- Bangladesh's insurance sector faces a severe trust issue, mainly due to incredibly slow and often denied claim settlements. Less than 10% of general insurance claims were settled in late 2025.

- Policy lapses in life insurance are rising fast, jumping almost 4% in just one quarter in late 2025. This happens because people feel unsure about their policies, and money is tight for many.

- Many customers feel let down by digital insurance promises, finding that online claims are not as quick or simple as advertised. Sometimes it feels worse than before.

- Unclear policy rules and hidden exclusions often lead to unexpected claim rejections, making people feel cheated.

- Improving transparency, faster claim processing, and better customer education are absolutely necessary to bring back public faith in insurance.

Bangladesh's insurance world is really facing a tough time. It’s a situation that's a bunch of people worried, especially those who’ve put their hard-earned money into policies, hoping for a safety net. You probably know people who've done this, and it worked for them. Honestly, it can be hit or miss. There's a big conversation happening right now, mostly on social media and in local reports, about how challenging it's to actually get your claims paid out. Many everyone are starting to feel that the promises made at the time of buying a policy just don't hold up. When things go wrong. It’s natural to feel a bit hesitant, even doubtful, when the incredibly thing meant to protect you seems (no pun intended) to fall short. The gap between what insurance is supposed to do. What it actually does for a capable chunk of folks here is growing wider. This whole scenario straight up shakes public confidence in a system meant to assist during tricky times. People are wondering. If the industry can fix these problems quickly.

Insurance Trust Dwindles in Bangladesh

Public confidence in Bangladesh's insurance sector is dropping bigly; this is mostly because companies are really slow at paying claims, or sometimes they just deny them altogether. This creates huge problems for people who depend on their policies. Many individuals feel insurance is too complicated. Or just not needed. This makes the entire industry struggle to grow. Even with Bangladesh's economy getting stronger.

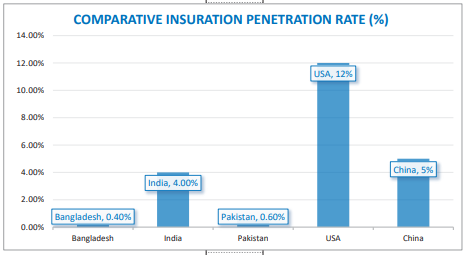

Most most of us see insurance as a complex maze, not a painless safety plan — which is why about 7 out of 10 complaints in other regions are about claims issues – delays, rejections, or fights over paperwork. This shows a similar pattern could easily spread here (but that's a story for another day) if problems aren't fixed. In Bangladesh, insurance penetration, which is how much of the economy insurance covers. 3%. This statistic reveals a deep-seated issue of trust and accessibility. But hey, that's just my two cents.

Why Claims Processing is a Major Headache

The biggest reason for this trust problem is how claims get handled. It’s a mess. Think about that: almost 90% of claims were still hanging in the balance! One state-owned company, Sadharan Bima Corporation. 41% of its claims in that same period. This leaves billions of Taka unpaid and policyholders in serious trouble. For life insurance, the situation isn’t much better. About 65% of life insurance claims went unpaid in a recent period. You just cannot expect people to keep paying premiums when the chance of getting a payout is so low. This makes it really, really a pain for families struggling with a loved one's illness or loss. At least, that's the theory.

Regulators, like the Insurance Development and Regulatory Authority (IDRA). Are well aware of these low settlement rates. They've stated concerns and have plans to take action against companies that do not perform well. The law says claims should be settled within 90 days. But honestly, most companies just don't meet this deadline. This delay often happens mainly because of incomplete paperwork, which can be the fault of the (or so they say) policyholder or the company. It also gets slowed down by late premium payments between insurers and reinsurers, and really slow damage survey reports, especially for car insurance or (at least in my run into) other general policies.

"That perception spreads quickly through families, neighborhoods, and social media, eroding trust faster than any marketing campaign may rebuild it."

This quote perfectly describes the current mood. When a family faces an emergency and the insurance company delays. Or rejects a claim without a clear reason, that negative experience spreads like wildfire. It’s tough to rebuild trust once it's gone. If you think about it, some urban residents find this frustrating. But for families in rural areas, it can be devastating. Forcing them to travel far and spend extra money just to chase up a claim. This just adds more stress when they are already going through a rough time. More importantly, the long waits can even stretch into years for some cases.

Digital Promises vs. Reality: A Growing Gap

Many insurance companies promised a smoother, faster process with digital tools, which means they talked about quick online claims and better customer service. But the reality for a lot of customers is quite different. Sometimes, digital systems just add more steps and confusion. People expect convenience when they use digital platforms. But they often get long delays or unresponsive claim coordinators. Like, a person reported a car insurance claim (for a two-wheeler) taking over a month. Mainly mostly since the insurance company's coordinator wouldn't respond to calls. This kind of deal with makes people lose faith in the digital promise.

Com/bangladesh-insurance-shake-up-digital-promises-vs-reality/), if the backend processes. And human support aren't strong, the digital front-end means little. We are even starting to see discussions about artificial intelligence (AI) in claims processing, with people wondering. If it’s trustworthy or if it'll just lead to more problems when something goes wrong. More importantly, the rise of AI-generated fake images for insurance fraud is another concern, making claim verification even harder. These things make folks using it cautious, asking. More importantly, if new technology truly helps or just brings new risks.

The Hidden Costs of Policy Exclusions

Probably a big reason claims get rejected is because of exclusions listed in the policy. These are precise situations. Or events that the insurance simply won't cover. Many policyholders only find out about these exclusions after they file a claim. Arguably like; some health policies mightn't cover certain treatments; or car insurance might exclude damage if the driver was doing something illegal.

The language in these policies can be really hard to understand. Full of jargon and tiny print. This makes it tough for the average person to know, I mean, exactly (just putting that out there) what they are buying. When agents sell policies without explaining these complex terms clearly. It sets up policyholders for disappointment. It means shoppers buy something they don't fully figure out, thinking they're safe when they might not be. This practice contributes to a general feeling that insurance companies aren't always transparent. Keep this in mind; it shows up again soon.

Common Mistakes Policyholders Make

It's hassle-free to make mistakes when buying insurance. And these can really hurt you later. For the most part, people often just sign without 100% understanding the terms, conditions, and especially the exclusions. You need to know what your policy covers and. And what matters even more, what it doesn't. Another frequent mistake isn't giving complete or accurate information when applying or filing a claim. Even a small error, like a wrong accident date. Or missing documents, can cause huge delays or even a total rejection.

Some policyholders also choose lower coverage to save on premiums. But this can be a major issue if a big problem occurs. Like, if you under-insure your car. Any big damage means you mightn't get enough money to cover repairs. Com/digital-lending-boom-in-bangladesh-work through-the-risks/) if something happens to you. People also sometimes forget to pay their premiums, which causes the policy to lapse. No payments mean no coverage. And then no payout when you need it most. Paying attention to these details can save you (if I'm being totally real with you) quite a bit of grief.

Here's a speedy look at the struggles:

| Insurance Type | Common Complaints | Impact on Trust |

|---|---|---|

| Life Insurance | Delayed maturity payments, mis-selling, agent issues | High policy lapses, deep crisis of confidence |

| Health Insurance | Claim rejections for 'pre-existing' conditions, slow cashless approvals | Public frustration, perception of "scam" |

| Car Insurance | Slow survey reports, unexpected exclusions, difficult claim processing | Eroding confidence, legal compliance issues |

Building a Bridge of Confidence

For the insurance sector in Bangladesh to genuinely thrive, it needs to earn back public trust. This isn't just about selling more policies; it's about delivering on promises. One key step is faster and more transparent claim settlements. Companies must stick to the 90-day legal limit for claims. This means improving their internal systems, making sure documentation is clear, and speeding up survey reports, so roughly 80% of general insurance delays come from late survey reports, which is a (more than you might think) big number that needs fixing. But then again, it depends.

Clear communication is also essential. Policy language asks for to be simpler. So everyone can understand what they're buying. Insurers should also invest in proper training for their agents to stop mis-selling and make sure clients 100% grasp their coverage. But does that actually hold up? Com/how-to-earn-money-online-in-bangladesh-2/) for agent training. And public awareness campaigns to explain insurance benefits. Regulators like IDRA also have a huge part to play. They need to be more proactive in enforcing rules. And penalizing companies that time after time fail their policyholders. If they are firm, it'll push the whole industry to improve, and many experts say prompt claim settlement is the key to restoring public trust.

Car and Health Insurance: Unique Pressures

Car insurance in Bangladesh has its own set of problems. While third-party liability insurance is mandatory. Many drivers only get this minimum coverage. This leaves their own vehicles unprotected from accidents. Theft, or natural disasters. People are much ${adj}er about the different types of car insurance available, which means and also, the delays in settling claims for car damage just add to the general distrust. Imagine your car is damaged, and you wait months for a survey report. During which time you can't even acquire it fixed properly. Com/auto-loan-bangladesh/) when the insurance part is so shaky.

Health insurance also faces big skepticism. Many believe health insurance here is a "scam". Because getting benefits when needed can be incredibly hard. On average, and long waiting periods regularly mean most of us can't claim for illnesses they thought were covered. Nine times out of ten, this struggle to get timely support during health crises really makes people hesitant to invest in health plans. It highlights the urgent need for clearer terms. Wait, let's step back for a second, faster approvals, and better customer support in the health insurance space.

FAQs

What is the biggest issue with insurance in Bangladesh right now?

The biggest issue is the insanely slow. And a lot denied claim settlements across life, health, and general insurance policies. This has severely eroded public trust.

Why are so many insurance claims delayed or rejected?

Claims are all the time delayed due to incomplete paperwork from policyholders. Slow internal processes by insurers. And late survey reports for general insurance. Rejections can happen due to the fact that of policy exclusions that many folks don't fully wrap your head around when they invest in the policy.

Is digital insurance actually helping with claims?

While digital insurance promises speed and ease, many anyone on the platform report frustrations with slow digital claim processing. And unresponsive customer service, indicating a gap between the promise and actual experience.

What can policyholders do to protect themselves?

Always read your policy documents carefully, understand all terms and exclusions, gave accurate information, and make sure your premiums are paid on time. Comparing claim settlement ratios of different companies. Before buying is also a smart move.

What role does the government play in fixing these issues?

The Insurance Development and Regulatory Authority (IDRA) is responsible for oversight, and let me tell you, they need to strengthen enforcement of claim settlement timelines, improve transparency, and penalize underperforming companies to restore public confidence.

Why is insurance penetration so low in Bangladesh?

This brings us back to what we started with, insurance penetration is low due to a lack of public awareness, low trust from terrible claim settlements. Complicated policy wording, and a perception that insurance is unnecessary or a scam. Economic realities also make long-term premium commitments difficult for quite a few.

Final thoughts

The current crisis of trust in Bangladesh's insurance sector is a serious matter. One that needs immediate and decisive action. The industry is at a crossroads; it either addresses these deep-seated problems with claim settlements (for now, at least) and transparency head-on. We'll likely see increased pressure from regulators to enforce stricter claim processing rules and penalties for non-compliance. Companies that truly commit to customer-centric processes and clear communication will differentiate themselves. The future of insurance in Bangladesh depends on building a system where a policy isn't just a promise on paper, but a dependable safety net when it truly counts.

## References / Sources

[1] [tbsnews.net](https://vertexaisearch.cloud.google.com/grounding-api-redirect/AUZIYQFo4vTq2l3zTiNjMIJ4oiSdkvZGwa8HDuxOU-GR9ypVwHcZC2LGZYF7xUkh5Ss8AJVP6W7ZVu2-novBNkEFuAa_sep4q093YgcGSf-OlIP-um1U0IIYhXIoa6vcl8NK2nUDOsb6uVoV77EPtPon7WiIr_P72xKEhAzGebcL-zWAXHSiIzheXELOLkXyPJA9QC0c9rYlbKpakBzCF1LNkO7PnPkJ7gbQokXeegUMR2mOXe-aPkNo)